High win rates can be misleading in SPX 0DTE options. Learn why expectancy and drawdown matter more in mechanical trading strategies.

When trading SPX 0DTE options, win rate gets a lot of attention. It’s common to hear traders brag about 85% or 90% win rates; but that number alone means very little. In fact, focusing on win rate can hide serious flaws in a trading system, especially in fast-moving, high-risk environments like zero-day SPX.

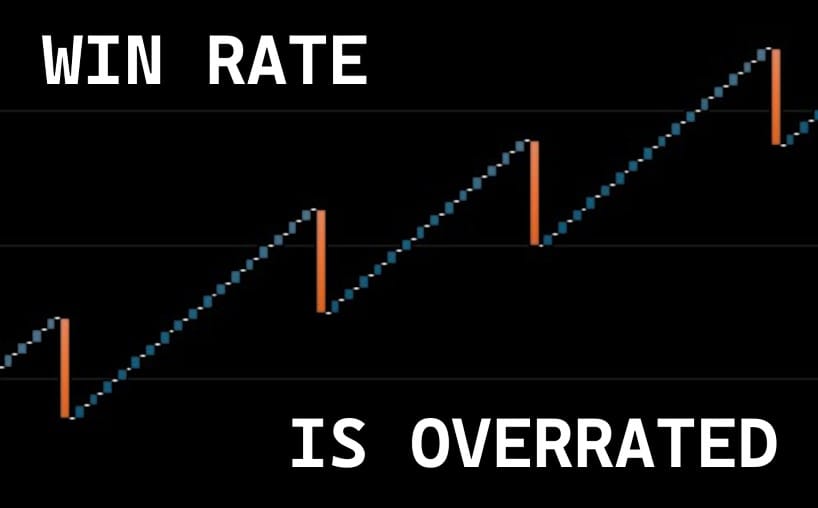

The Problem With High Win Rates

High win rate systems often rely on small, frequent gains while exposing traders to occasional large losses. One market spike can erase weeks of profits. If your system wins 9 out of 10 trades for $1.00, but the 10th trade loses $5.00, your “high win rate” is covering up a negative expectancy.

Better Metrics: Expectancy and Profit Factor

Expectancy measures your average profit per trade:

(Win% × Avg Win) – (Loss% × Avg Loss)

This single number shows whether your system actually makes money over time.

Profit Factor (total profit ÷ total loss) gives similar insight. If your profit factor is under 1.0, even with a 90% win rate, you’re losing money.

Mechanical Systems Need Resilience

SPX 0DTE systems thrive on consistency and limited exposure. That’s why many successful traders favor narrower verticals rather than using stop losses. Wider spreads and emotional trade exits often magnify damage when volatility hits. The key is to cap risk mechanically, not emotionally.

Mechanical strategies must survive the outliers; days with violent reversals or news-driven volatility. A system built on fragile win-rate math won’t hold up.

Final Thoughts

A high win rate feels good but proves nothing. What matters is how much you win when you're right, and how much you lose when you're wrong. Expectancy, profit factor, and max drawdown tell the real story.

If you're running mechanical SPX systems, focus on risk-adjusted performance, not vanity metrics.

📚 Explore More

Dig deeper into edge and system design in our post: