The Hidden Challenges of Backtesting Options Trades

Backtesting is a crucial step in refining any trading strategy, especially when it comes to options. However, in my experience, many of the pitfalls—or "gotchas"—in backtesting options come down to two critical aspects: data frequency and volatility management. If not carefully addressed, these issues can lead to misleading results that don't hold up in live trading.

The Importance of High-Frequency Data

One of the most overlooked aspects of options backtesting is the frequency of the data. Options prices can move rapidly, and relying on minute-level data (or even less frequent snapshots) can result in missed critical price movements. For instance, a price might have briefly moved near a profit target, but without sufficient data resolution, that nuance may be lost. This can lead to backtests that either miss trades entirely or incorrectly assume a profit target was realistically hit.

To mitigate this, I recommend using tick-level or at least second-level data. This higher resolution provides a more accurate view of how prices behaved within the trading session. While higher-frequency data can be heavier and more complex to process, it ensures that backtests capture the true dynamics of the market.

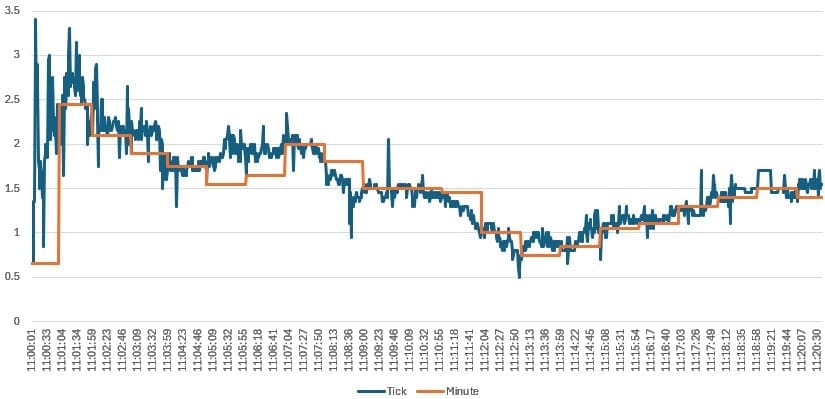

A side-by-side graph comparing a minute-level data chart versus a tick-level chart, illustrating how critical price movements can be missed in lower-frequency data.

Navigating the Volatility Trap

Another major challenge is dealing with volatility in pricing, particularly when gamma exposure is high. Gamma, as you know, measures the rate of change in delta for an option. When gamma is elevated—especially for short-dated options like SPX 0DTE trades—price swings can be dramatic and frequent.

Here's the problem: A sharp price spike can momentarily breach your stop-loss, and in real trading, such a spike could realistically trigger an exit. However, for profit targets, a spike might falsely indicate a successful trade in backtesting, when it wouldn’t realistically allow enough time for an exit in real market conditions. The market depth, order flow, and execution speed all play roles that backtesting algorithms can't fully simulate.

To address this, I use a moving average approach specifically for profit targets. I rely on a 5-second average to trigger exits on the profit side. This method helps smooth out noise and ensures that only sustainable price levels trigger exits. On the stop-loss side, however, I allow raw price spikes to trigger exits. This conservative approach ensures that my backtests don't overestimate profitability and account for realistic worst-case scenarios.

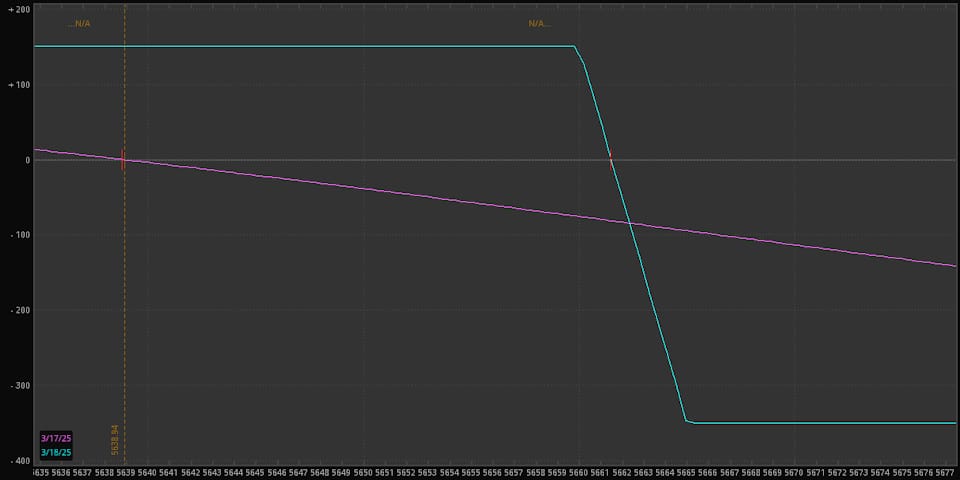

A graph showing a price spike momentarily clearing the PT line, but with the 5-second moving average remaining below it. This would visually demonstrate the importance of smoothing in avoiding false exits.

Why Conservative Triggers Matter

This approach ties into the broader philosophy of conservative backtesting. It's better to be slightly pessimistic in simulations than to be caught off guard in live markets. Beyond using moving averages for profit targets, I also apply conservative rounding when combining prices to create vertical spreads. Since most brokerages require options prices to be divisible by 0.05, I round buys up and sells down. This practice accounts for less favorable pricing scenarios, ensuring that the backtest doesn't falsely assume more optimistic fills than what would be realistic.

Additionally, I treat stop-losses using the worst-case execution price to avoid underestimating risk. By using average prices for profit-taking and worst-case prices for stop-losses, the backtest reflects a more cautious and realistic trading environment. This practice doesn't just reduce over-optimism; it also forces you to build strategies that can withstand real-world frictions like slippage, spread widening, and execution delays.

| Data Frequency | Pros | Cons |

|---|---|---|

| Minute-Level | Lower data volume, faster processing | Misses short-term spikes and critical moves |

| Second-Level | Captures more price movements accurately | Larger data sets, increased processing time |

| Tick-Level | Most accurate representation of price action | Very large data sets, highest processing demand |

Final Thoughts

Backtesting is as much an art as it is a science. It's about creating simulations that are both rigorous and realistic. By focusing on high-frequency data and implementing conservative, volatility-aware exit triggers, you can avoid many of the common pitfalls that lead to inaccurate results.

In the end, the goal is simple: Build strategies that perform in the chaos of the live market, not just in the perfection of historical simulations. Getting the details right in backtesting is one of the best ways to ensure success when real money is on the line.

If you've got any thoughts or methods you've used to tackle these challenges, I'd love to hear about them. Backtesting isn't just about numbers—it's about learning from experience and refining the craft.